- Contact EquityLine Mortgage Investment Corporation

- (416) 999-3993

- info@EquityLineMIC.com

In 1973, the Government of Canada introduced legislation to address a chronic shortfall in mortgage funding across the country. Because of rapid population growth and other factors, there was an annual projected gap, at that time, of $2.3 billion between funds needed and funds available for residential and commercial real estate mortgages nationwide. An important part of the government’s solution was to create a new class of financial instrument: the Mortgage Investment Corporation (MIC).

MICs were designed to meet two key objectives:

1. Provide qualified borrowers (individuals, developers) with an alternative to traditional mortgages through a loan facility mechanism with less rigid terms and conditions than financial institutions generally impose.

2. Provide private investors with a safe mechanism and regulated way to invest in mortgage loans with terms between 6 and 36 months at considerably higher rates than most financial institutions offer.

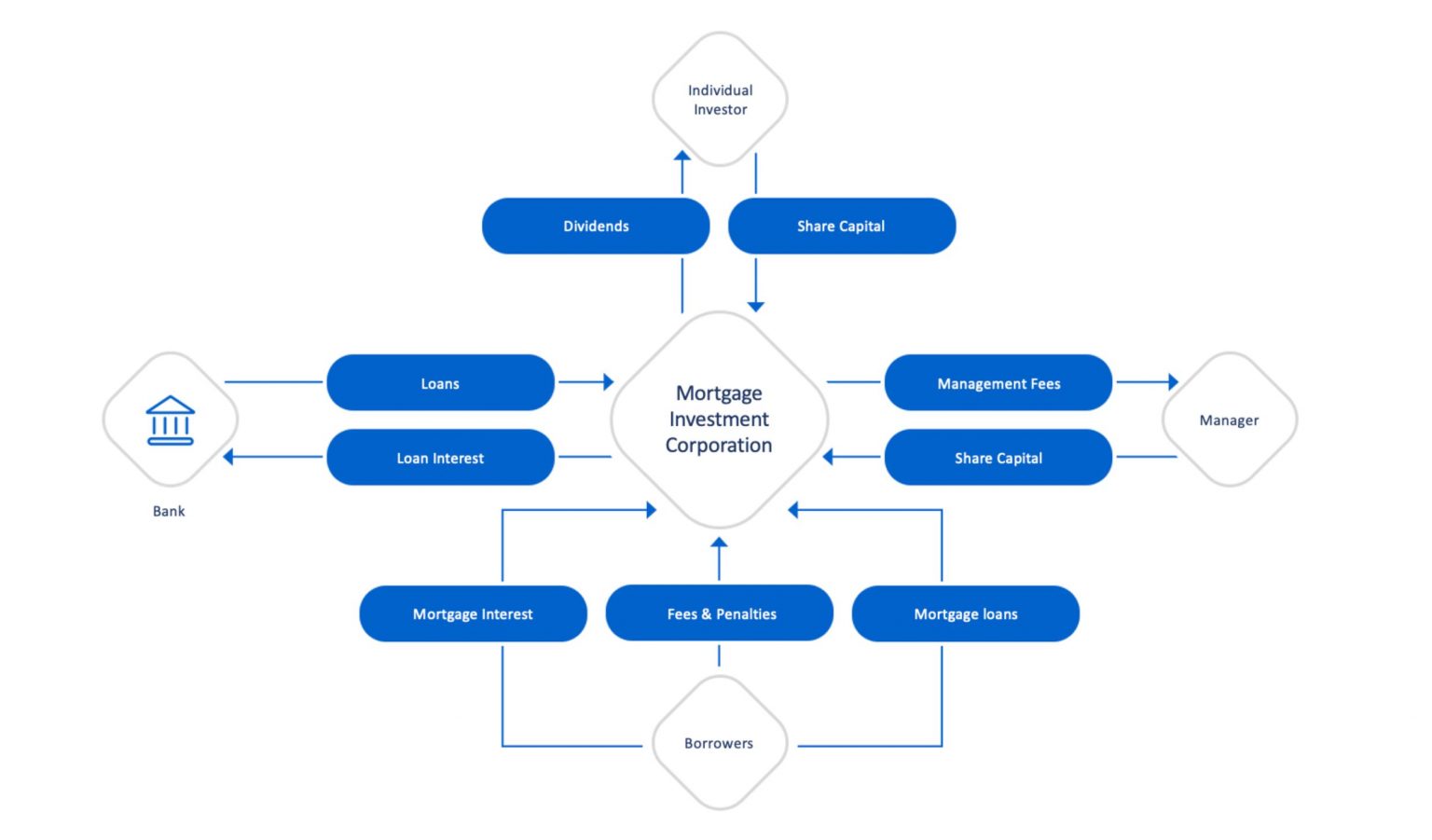

MICs are now firmly established in Canada as investment and lending corporations geared specifically towards mortgage lending. Investors pool their money by buying shares in a MIC, and the MIC lends those funds to borrowers who provide their real estate as security.

Governed by Section 130.1 of the Income Tax Act, MICs pay no corporate tax and act as flow-through entities. They must pay out all their taxable income in the form of dividends.

For tax purposes, a MIC’s dividends are treated as interest income in the hands of the shareholders. Shares of a MIC are eligible investments under the Income Tax Act for RRSPs, RRIFs, DPSPs, RESPs and TFSAs.

Mortgage Investment Corporations:

Uniquely Canadian & Globally Available

The management of a MIC is responsible for all aspects of the MIC’s operations, including sourcing suitable mortgage investments, analyzing mortgage applications, negotiating applicable interest rates, terms and conditions, instructing solicitors, managing the mortgage portfolio and general administration.

Like an investment fund, the manager of a MIC receives a management fee, typically calculated as a percentage of assets under administration. EquityLine’s management fee of .5% to 1% is among the lowest in the industry.

Please speak with your Financial Advisor or Dealing Representative about EquityLine MIC. If you do not have a Financial Advisor or Dealing Representative, please contact us and we’ll connect you with one.

Please speak with your Financial Advisor or Dealing Representative about EquityLine MIC. If you do not have a Financial Advisor or Dealing Representative, please contact us and we’ll connect you with one.